We are pleased to republish the below article by the distinguished Marxist economist Michael Roberts, which looks at the reality of the Chinese economy and its prospects in the context of the adoption in March of the 15th Five-Year Plan, by the country’s highest legislative body, the National People’s Congress (NPC).

Adopting the Marxist standpoint of seeking truth from facts in his economic analysis, Michael deals with a number of erroneous claims often made regarding the Chinese economy in a rigorous but comprehensible fashion, which also does not shy away from some of the very real challenges it faces.

He sees the economic growth target set for this year of around 4.5-5% as being well justified and goes on to explain:

“In 2025, China’s real GDP growth was 5%, a rate among the major economies of the world only surpassed by India (which exaggerates its GDP data) and more than twice the US growth rate and three times that of the rest of the top G7 capitalist economies.

“Since 2020, the government has set a target for China to become a ‘mid-level’ economy, (as defined by the World Bank at $20,000 per person at 2020 prices) by 2035. That meant effectively doubling its per capita GDP over those 15 years. It is clearly on target to do that as China’s per capita income would need to grow only at an average annual rate of about 4.17% a year from hereon. Assuming China averages an annual real per capita GDP growth rate from hereon of about 4.5%, then it will surpass the World Bank definition by 2034.”

Making an important comparison, he further notes: “China’s per capita GDP would still be only 27% of that of the US (assuming the US per capita GDP grows at a 1.5% average rate from here). In contrast, India’s per capita GDP would be only 5% of the US by 2035.”

He then proceeds to deal with the fact that: “China’s GDP and growth rates are continually dismissed by many mainstream Western economists as well as by some on the heterodox left,” but points out:

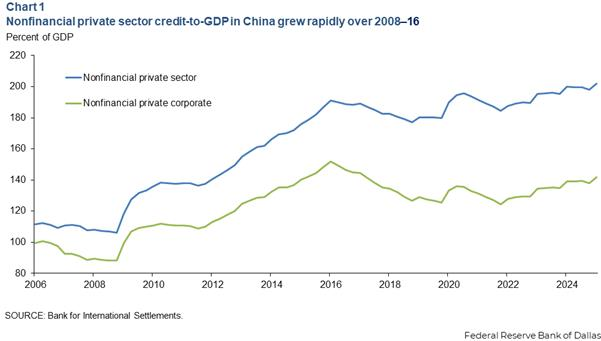

“Recently the prestigious Penn World Tables have confirmed that they consider China’s growth data as broadly accurate and no longer attempt to ‘adjust’ it downwards… Yes, corporate debt is high, and the property market is still falling. But nearly all this debt is financed entirely from domestic savings, unlike many examples of rapid credit expansion elsewhere. So, this debt is perfectly manageable.”

He also deals with the balance and relationship between investment and consumption, another issue on which a measure of confusion abounds:

“China’s household consumption is not stagnating, it’s growing 4.4%, more or less in line with GDP growth. Exports are not driving growth. Net trade accounted for about 20% of 2025 growth, the rest was driven by domestic consumption and investment.”

Having outlined China’s considerable progress in developing renewable energy – while also noting the country’s real difficulties if it is to meet its ambitious climate goals – he notes:

“China’s economy is now driven by technological investments, no longer by low-value manufactured goods or unproductive investment in real estate. Now it is what Chinese economic strategists call the ‘new quality productive forces’. More electric vehicles are on the road in China than in the US and Beijing’s roll-out of 5G telecommunications networks has been much faster. China’s home-grown airliner, the C919, is on the cusp of mass production and appears ready to enter a market currently dominated by Boeing and Airbus. The BeiDou satellite navigation system is on par with GPS in coverage and precision.”

In a measured and balanced way, he notes that: “China still has a long way to go. By the end of the new National Plan, living standards for average Chinese households will have improved significantly, but China’s per capita income and productivity levels will still be well below those in the G7 economies. Moreover, what will be an issue is finding employment for young people with qualifications, as automation replaces labour in an increasingly hi-tech industrial economy. Already, youth unemployment is high.”

Michael also adopts this approach to the vexed question of inequality in China – recognising the problem but contextualising it, including within an international comparative framework:

“China has a high level of inequality of incomes by international standards, although it is still lower than many other ‘emerging’ economies like Brazil, Mexico or South Africa – and the Gini inequality ratio peaked just before the Great Recession and has been falling since. The main reason for the high inequality ratio is the disparity of incomes between urban and rural workers and between the wages in coastal and inland cities, as well as educational qualifications.

“When it comes to inequality of personal wealth, China is not so unequal as many of its economic peers. The Gini inequality of wealth ratio is much higher in Brazil, Russia and India, and higher in the US and Germany.”

Much the same may be said with regard to millionaires and billionaires, another oft cited concern regarding China:

“Given the size of the population, millionaires in China remain relatively rare: about one for every 200 adults i.e. 0.5%. Millionaires account for 3% of adults in Italy and Spain; France, Austria or Germany about 4%; around 6% in social democratic Scandinavia; above 8% in the US and Australia and highest of all in Switzerland (15%).”

Concluding he expresses the view that: “The key to China’s economic success is its large state sector that can drive investment and so implement national plan targets. It shows the value of public ownership and dominant government-directed investment within a national plan.”

Elaborating his view, he writes: “China is not a socialist country, but neither is it capitalist.”

This raises an interesting and important point. If by this, Michael means that China is not yet a fully developed socialist country, in which the vestiges of previous exploiting class societies have been almost entirely extirpated, then there would seem to be little difference between his view and that of the editors of this website. And moreover, and far more importantly, not with the analysis put forward by the Communist Party of China (CPC). It is precisely for this reason that the CPC has long since advanced the view that China is still in the primary stage of socialism. This in turn is based on, and builds on, the scientific socialist view that socialism, properly understood, is precisely a transitional form of society between capitalism (or indeed pre-capitalist social formations as the unfolding of history has revealed) and communism, and therefore contains features of both its future and its past and furthermore itself embodies many stages, phases and national forms. In a sense, Michael’s view that China is “not capitalist” (rather than it allegedly also being “not socialist”) is, to paraphrase Mao, the key link that once grasped allows all else to fall into place. It is a welcome and essential line of demarcation with much of contemporary Trotskyism, this being the trend in Marxism with which Michael has long been associated.

It would be remiss of us, however, not to note that this political legacy, in our view, leads Michael to express some opinions with which we do not agree. At the start of the article, he essentially dismisses the role of China’s legislative bodies, for example claiming that “in reality, it [the NPC] merely approves what the leading CP elite have already decided in advance.” In his conclusions he goes further and casually refers to “the autocratic Communist leadership”. The comparison between his skillful Marxist analysis of economics and his occasional forays into political phrasing that would not be found jarring in the right-wing media is somewhat striking.

As we have analysed and explained on many occasions, most recently here, the fact that proposals put to the NPC are generally approved by an overwhelming majority rests on a number of factors, including the fact that they are discussed, debated and amended at all levels from the grassroots up before final approval. As this is a process of nation building and socialist construction, the focus is on consensus not confrontation. It is of course correct (and certainly no secret) to note that the details generally presented to the NPC are first approved by the Communist Party.

An October 30, 2025 article, published on the website of China’s State Council presents a detailed overview of how this worked in the case of the Five-Year Plan that was finally adopted nearly five months later:

“To better understand public needs and expectations, six research teams were dispatched to 12 provincial-level regions. They met with local officials and visited 66 primary-level organisations, including enterprises, communities and schools.

“From May to June, entrusted by Xi, senior Party leaders held three symposiums to solicit views from experts in the economic and sci-tech sectors, as well as representatives from the grassroots.

“Around the same time, public opinions were solicited on the new plan during a month-long online consultation campaign. The initiative drew over 3.11 million valid submissions, yielding more than 1,500 constructive suggestions across 27 topics…

“In early August, the draft text was discussed by selected Party members. Later that month, Xi chaired a symposium to hear views from non-CPC personages on the draft.

“By September, a total of 2,112 suggestions had been collected from various regions, departments and sectors, resulting in 218 revisions to the document.”

This is what Xi Jinping refers to as whole process people’s democracy. This in turn has deep roots in Chinese revolutionary theory and practice, as set out for example in this 1943 article by Comrade Mao Zedong:

“In all the practical work of our Party, all correct leadership is necessarily ‘from the masses to the masses’. This means: take the ideas of the masses (scattered and unsystematic ideas) and concentrate them (through study turn them into concentrated and systematic ideas), then go to the masses and propagate and explain these ideas until the masses embrace them as their own, hold fast to them and translate them into action, and test the correctness of these ideas in such action. Then once again concentrate ideas from the masses and once again go to the masses so that the ideas are persevered in and carried through. And so on, over and over again in an endless spiral, with the ideas becoming more correct, more vital and richer each time. Such is the Marxist theory of knowledge.”

This is indeed quite different from bourgeois democracy, famously described by Lenin, paraphrasing Marx, as: “The oppressed are allowed once every few years to decide which particular representatives of the oppressing class are to represent and repress them.” Precisely for this reason, it is neither “symbolic” nor “authoritarian”.

This important difference notwithstanding, we have the highest respect for Michael’s work and believe that this article is worthy of wide and serious study. It was originally published on his blog, The Next Recession, on March 8.

The Chinese government is just completing its annual ‘two sessions’ or lianghui. The ‘two sessions’ refers to two major political gatherings: the Chinese People’s Political Consultative Conference (CPPCC), a political advisory committee; and the National People’s Congress (NPC), China’s top legislative body. These are ostensibly not meetings of the Communist Party, but instead are meetings of the Chinese state. The consultative meeting is largely symbolic, with leading business and local leaders appearing for pre-arranged discussions. The real focus is the NPC, which officially decides economic policy. In reality, it merely approves what the leading CP elite have already decided in advance. With around two-thirds of its members belonging to the Communist Party, the NPC has never rejected a bill proposed by the party.

This year’s Two Sessions was different in that, apart from approving economic policies for this year, it also agreed to the 15th National Plan to take the Chinese economy up to end of this decade.

First, it decided to set a target of around 4.5-5.0% in real GDP growth for 2026. This was the first time since 1991 that the target figure dropped below 5%. Prime Minister Li, in presenting the economic targets, explained that the target was lower because of uncertainties in world trade and geopolitics. Even so, the growth target was modest and the leadership felt confident that it would be met.

There is good justification for that view. In 2025, China’s real GDP growth was 5%, a rate among the major economies of the world only surpassed by India (which exaggerates its GDP data) and more than twice the US growth rate and three times that of the rest of the top G7 capitalist economies.

Since 2020, the government has set a target for China to become a ‘mid-level’ economy, (as defined by the World Bank at $20,000 per person at 2020 prices) by 2035. That meant effectively doubling its per capita GDP over those 15 years. It is clearly on target to do that as China’s per capita income would need to grow only at an average annual rate of about 4.17% a year from hereon. Assuming China averages an annual real per capita GDP growth rate from hereon of about 4.5%, then it will surpass the World Bank definition by 2034.

China’s per capita GDP would still be only 27% of that of the US (assuming the US per capita GDP grows at a 1.5% average rate from here). In contrast, India’s per capita GDP would be only 5% of the US by 2035. For more on catching up, see my paper here. When it comes to GDP growth, the size of an economy matters a lot. In 2025, China’s GDP rose 5% or $970 billion. To match that this year, China only needs to achieve 4.75% GDP growth. In contrast, officially India grew 7.6% in 2025 or just $326bn. So India’s GDP rose three times less than China. For India to grow as much as China in $bn, it would need to grow at roughly 25% in a single year. Mass counts.

China’s GDP and growth rates are continually dismissed by many mainstream Western economists as well as by some on the heterodox left. They argue two things. First, the China’s statistical data is faked or incorrect; and second, that China’s economy is going to slow towards stagnation because of overwhelming debt, a property market collapse and declining productivity growth – similar to what has happened to Japan since the 1980s. I have dealt with both of these arguments in many previous posts here and here. But I can now add that recently the prestigious Penn World Tables have confirmed that they consider China’s growth data as broadly accurate and no longer attempt to ‘adjust’ it downwards.

As for debt and the property market, y Yes, corporate debt is high and the property market is still falling. But nearly all this debt is financed entirely from domestic savings, unlike many examples of rapid credit expansion elsewhere.

So this debt is perfectly manageable. As for the post-COVID property meltdown, the latter is gradually reducing its drag on the economy.

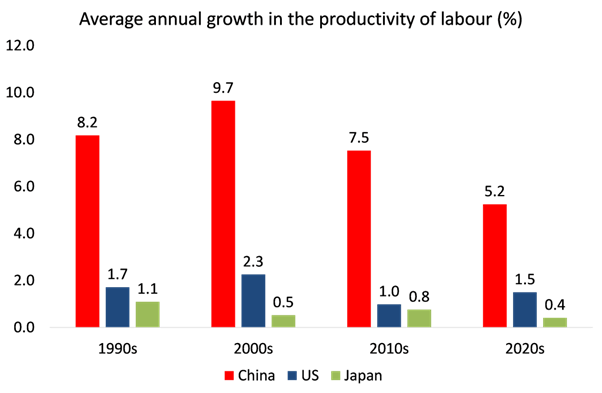

Productivity growth is key in an economy where the working age population is declining. It has fallen from previously heady heights, but it still stays significantly higher than in the advanced capitalist economies.

Western economists continually demand that China a) stop manufacturing exports as the main driver of growth; 2) stop ‘unfairly’ subsiding those exports that outcompete competitors; and 3) instead increase domestic personal consumption and reduce saving and investment. The most recent example of these policy demands comes from the IMF: “China cannot count on ever higher exports to drive durable growth in the coming years. That makes pivoting to consumption-led growth the overarching policy priority.”

I have dealt with these demands in several previous posts. But let’s briefly reiterate. China’s household consumption is not stagnating, it’s growing 4.4%, more or less in line with GDP growth. Exports are not driving growth. Net trade accounted for about 20% of 2025 growth, the rest was driven by domestic consumption and investment. Fast growth in productivity has avoided inflation and is not due to a ‘lack of domestic demand’. Why should China change from its investment-led economy that has seen the average real wage in urban areas grow by 2,406% since 1978 taking purchasing power up 25 times? Can the consumption-led economies of the US and the UK match that rise in purchasing power for their households?

As for ‘unfair’ subsidies applied to China’s industry, a recent report concluded that “While China is indeed an active user of industrial subsidies, direct fiscal support has stabilised since 2008. The strategic focus has shifted decisively from attracting foreign investment towards promoting domestic innovation and technological capabilities. Manufacturing subsidies, contrary to common perception, are relatively modest and decentralised.”

Take motor vehicles. China’s BYD and Musk’s Tesla both make EVs in China. Yet BYD has significantly lower costs. Vertical integration is very high for BYD and research and development is far cheaper. State subsidies are only a small part in reducing costs.

In its targets, the 15th National Plan follows on closely from the 14th just finished. And it is a real plan, more than just a guide or aspiration. Many of the objectives are considered mandatory or binding and so must be implemented.

In the latest plan, of the 20 or so indicators, the emphasis has shifted towards raising the standard of living and less so on economic development.

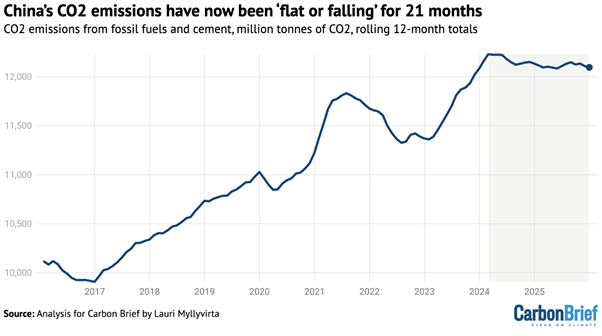

Green development is still important. China’s carbon dioxide (CO2) emissions fell by 1% in the final quarter of 2025, likely securing a decline of 0.3% for the full year as a whole.This extends a “flat or falling” trend in China’s CO2 emissions that began in March 2024 and has now lasted for nearly two years.

The CO2 numbers imply that China’s carbon intensity – its fossil-fuel emissions per unit of GDP – fell by 4.7% in 2025 and by 12% during 2020-25. But this is still short of the target of an 18% reduction set in the last five-year plan. China now needs to cut its carbon intensity by around 23% over the next five years, but the 15th plan only aims at reducing China’s carbon intensity by 17% by the end of this decade. So China is set to fall short of meeting its very ambitious 2030 target of cutting carbon intensity by 65% by 2030.

China’s solar industry has been a poster child for the country’s economic rise over the last four decades. The output of Chinese solar grew by 76% annually between 2004 and 2013. At the same time, the cost of solar has fallen by over 90%, making it competitive with fossil fuels. Subsidies to produce, install and perform solar R&D were a major cause of Chinese industry’s explosive growth. Last year was the first year ever that energy storage capacity – mainly batteries – grew faster than China’s peak electricity demand in 2025 and faster than the average growth in the past decade.

China’s economy is now driven by technological investments, no longer by low-value manufactured goods or unproductive investment in real estate. Now it is what Chinese economic strategists call the “new quality productive forces”. More electric vehicles are on the road in China than in the US and Beijing’s roll-out of 5G telecommunications networks has been much faster. China’s home-grown airliner, the C919, is on the cusp of mass production and appears ready to enter a market currently dominated by Boeing and Airbus. The BeiDou satellite navigation system is on par with GPS in coverage and precision.

China also beats the US in industrial robot density, with 470 robots installed per 10,000 employees in 2023 compared with 295 in the US. China is also about to match the US in patents with its global share rising from 4% in 2000 to 26% in 2023, while the US share dropped by more than 8% points. And China’s semiconductor production is now one-quarter of global output compared to 16% in the US and 7% in Europe.

{kind=link}

China still has a long way to go. By the end of the new National Plan, living standards for average Chinese households will have improved significantly, but China’s per capita income and productivity levels will still be well below those in the G7 economies. Moreover, what will be an issue is finding employment for young people with qualifications, as automation replaces labour in an increasingly hi-tech industrial economy. Already, youth unemployment is high.

And China has a high level of inequality of incomes by international standards, although it is still lower than many other ‘emerging’ economies like Brazil, Mexico or South Africa – and the gini inequality ratio peaked just before the Great Recession and has been falling since. The main reason for the high inequality ratio is the disparity of incomes between urban and rural workers and between the wages in coastal and inland cities, as well as educational qualifications.

When it comes to inequality of personal wealth, China is not so unequal as many of its economic peers. The gini inequality of wealth ratio is much higher in Brazil, Russia and India, and higher in the US and Germany. According to the latest estimates, the top 1% of wealth holders in China take 31% of all personal wealth compared to 58% in Russia, 50% in Brazil, 41% in India and 35% in the US. This is a good measure of the economic power of the top elite and oligarchs in these countries.

Much is made of the number of millionaires and billionaires in China. But given the size of the population, millionaires in China remain relatively rare: about one for every 200 adults ie 0.5%. Millionaires account for 3% of adults in Italy and Spain; France, Austria or Germany about 4%; around 6% in social democratic Scandinavia; above 8% in the US and Australia and highest of all in Switzerland (15%). China has had rapid growth in this top wealth tier. But while it has more than four times as many people as the US, the number of high net-worth Americans is 4.8 times greater than the number in China. And the inequality of wealth in China is centred on property, not financial assets (so far), unlike the main capitalist economies of the G7. And that is because finance has not been fully opened up to the capitalist sector.

In my view, the key to China’s economic success is its large state sector that can drive investment and so implement national plan targets. It shows the value of public ownership and dominant government-directed investment within a national plan. As a result, China has avoided any recession or slump in the last 50 years, even during COVID, even though there have been many errors and zig zags in economic policy by the autocratic Communist leadership. China is not a socialist country, but neither is it capitalist. I explain that conundrum here.

I got caught with the discussion of ‘GDP’. This is frankly a very poor measure of prosperity as it ignores the importance of production. In America, GDP is weighted with what Michael Hudson calls “economic rent,” also thought of as ‘unearned income’. This kind of economic activity is the opposite of production and is better measured as a subtrahend, an expense in accounting, and should be subtracted from real GDP. So Goldman Sachs traders make billions but their ‘work’ is functionally meaningless. Worse are financial fees and high interest that poor people have to pay on their credit cards. Unearned income and financial rent are what JS Mills called “making money in your sleep,” and is properly the work of a parasite.

If China wanted to raise GDP American style quickly, she would just get masses of people indebted so they pay interest and high rent. But she won’t do so.